Construction Cost Insights Report Q2 2026

Produced in partnership with Building Design+Construction, the Construction Cost Insights Report uses Gordian’s RSMeans™ Data construction costs and internal expertise, along with perspectives from industry leaders to evaluate the short-term and long-term cost trajectory of prominent construction materials and offer a range of perspectives on challenges in the marketplace.

This quarter’s report comes at a time of high uncertainty and low confidence. Fuel costs are through the roof and rising seemingly by the minute. Long lead times are rampant. No one is quite sure what will happen next. The Q2 2026 Construction Cost Insights Report is packed with data-driven analysis and field observations that help you find stability amidst the chaos.

Download the Q2 report for:

- In-depth material cost analysis, including which costs are accelerating and which are stabilizing.

- Discussion of how data center construction is spiking certain costs and squeezing the supply chain.

- Proactive procurement strategies for reducing long lead times, particularly within freight-sensitive and high-demand sectors.

Introduction

Construction cost conditions entering Q2 2026 reflect a market experiencing renewed pricing pressure across several key material categories, particularly metals and electrical system products. Drawing on Q2 2026 cost data from Gordian’s RSMeans™ database, along with perspectives from industry professionals at STO Building Group and Robins & Morton, the data indicates that material costs increased at a faster pace than installation costs during the quarter, signaling a shift from the more labor-driven escalation patterns seen earlier in the year.

Structural steel, copper wire and conduit all experienced notable increases during the quarter, while concrete block and several other material categories remained comparatively stable. Contractors and suppliers report that cost escalation is being shaped less by broad-based increases across all categories and more by concentrated pressure tied to energy costs, transportation, manufacturing capacity and sector-specific demand.

Healthcare, infrastructure and data center construction activity continues to impact both procurement planning and labor availability in several regions. Industry participants report ongoing challenges tied to long-lead electrical and mechanical equipment, specialized labor shortages and freight-sensitive materials, particularly within technology-focused and high-growth sectors.

Contractors across multiple sectors are also adapting procurement and risk-management strategies in response to uneven market activity. Early procurement planning, supplier diversification, escalation planning and alternative material evaluations are playing an increasingly important role in managing schedule and budget exposure tied to cost variability and material availability.

While many traditional construction materials have shown signs of stabilization compared to the sharp volatility experienced in recent years, pricing trends are still expected to vary significantly by material category, geographic region and project type through the remainder of 2026.

Q2 2026 pricing data reflects a construction market that is once again experiencing selective cost acceleration, with metals and electrical system materials driving much of the upward movement.

Cost increases have been concentrated in structural steel, copper wire and conduit, reflecting renewed upward movement across metals and electrical system materials. Copper products posted some of the strongest annual increases among tracked categories, while steel pricing rebounded sharply entering Q2.

Building Models Used to Calculate Price Data

Gordian’s data team researches material, labor and equipment prices and quantities in cities across the U.S. and Canada to create a composite cost model, which is weighted to reflect actual usage in the building construction industry. To capture the types of construction activity typically performed across North America, researchers merged nine building types, which represent those most commonly found across America and Canada. They are:

- FACTORY (one story)

- OFFICE (two to four stories)

- STORE (retail)

- TOWN HALL (two to three stories)

- HIGH SCHOOL (two to three stories)

- HOSPITAL (four to eight stories)

- GARAGE (parking)

- APARTMENT (one to three stories)

- HOTEL/MOTEL (two to three stories)

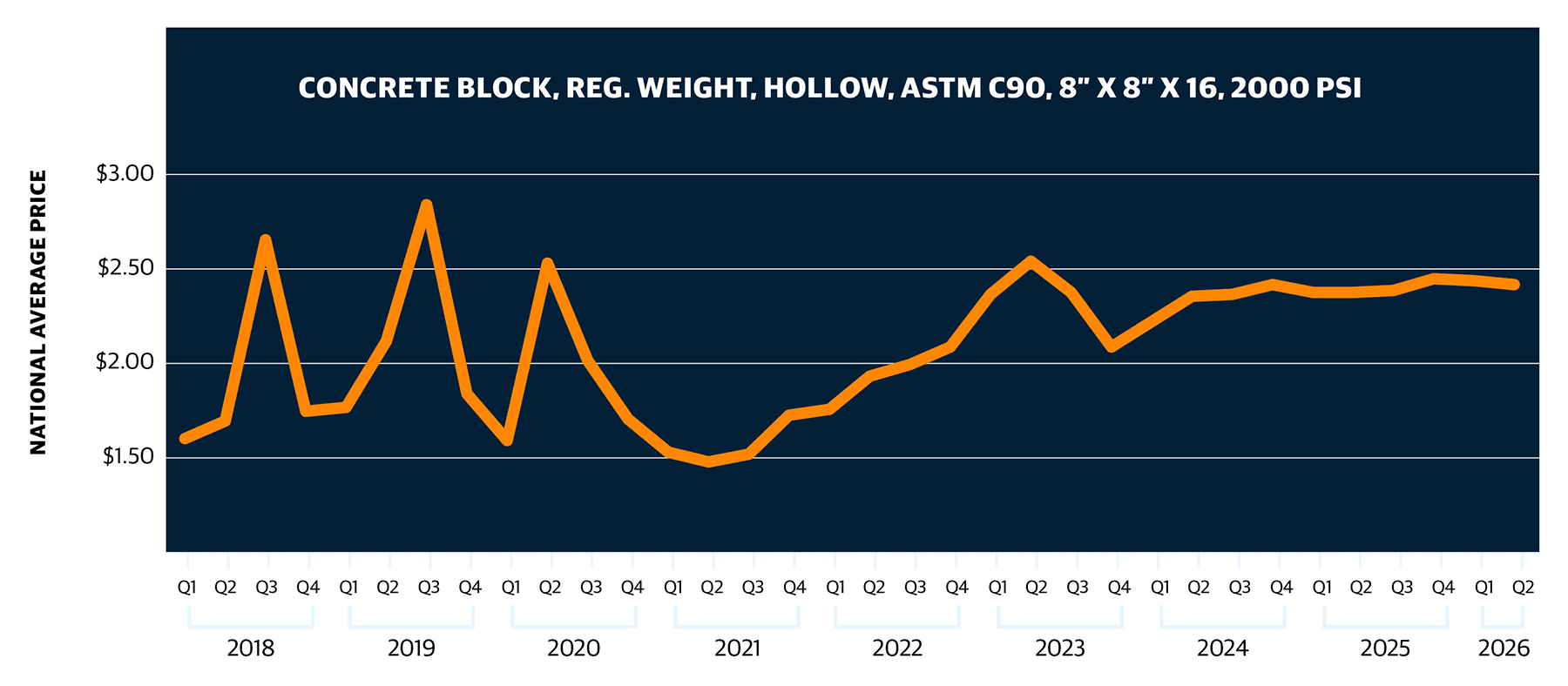

By contrast, concrete block pricing remained comparatively stable during the quarter, reflecting lower volatility than many metal-based products. Fiberglass insulation pricing has also remained relatively steady in recent months, though year-over-year comparisons continue to reflect elevated manufacturing and input costs from prior periods. Framing lumber pricing increased moderately during the quarter, suggesting a more balanced supply-and-demand environment than the volatility seen in recent years.

How National Average Material Costs Are Determined

Gordian’s team contacts manufacturers, dealers, distributors and contractors all across the U.S. and Canada to determine national average material costs. Included within material costs are fasteners for a normal installation. Gordian’s engineers use manufacturers’ recommendations, written specifications and/or standard construction practice for size and spacing of fasteners. The manufacturer’s warranty is assumed. Extended warranties and sales tax are not included in the material costs.

Note: Adjustments to material costs may be required for your specific application or location. If you have access to current material costs for your specific location, you may wish to make adjustments to reflect differences from the national average.

Adam Raimond, Program Manager, Construction Indices at Gordian, attributes much of the recent fragmentation across materials to rising energy and transportation costs, along with uneven manufacturing activity and concentrated demand within specific sectors. In particular, energy-intensive products such as steel and other metal-based materials have experienced renewed cost escalation entering 2026.

Industry analysis from STO Building Group — including insights from David Hamilton, Senior Vice President, Construction Procurement Solutions, and Doug Allen, Manager, Strategic Growth & Corporate Development — points to growing volatility across metals, electrical equipment and freight-sensitive materials.

In its latest procurement market update, STO notes that extended lead times for switchgear, transformers and other electrical equipment are still influencing procurement planning, especially in high-demand sectors such as healthcare, infrastructure and data centers.

In This Quarterly Construction Insights Report:

In this Quarterly Construction Cost Insights Report, we will be examining key data points surrounding construction material pricing. We will look at the Historical Cost Index, offering a retrospective lens on pricing trends, and the City Cost Index, providing a granular view of localized market variations. In addition, we will thoroughly explore the pricing trends of six key building materials:

- STRUCTURAL STEEL

- FRAMING LUMBER

- CONCRETE BLOCK

- CONDUIT

- COPPER ELECTRIC WIRE

- FIBERGLASS INSULATION

Robins & Morton reports seeing similar conditions across healthcare and technology-focused construction projects in the southern United States. According to Tom Thibeaux, Preconstruction Division Manager at Robins & Morton, competition with data center construction is affecting pricing and availability across mechanical, electrical, plumbing and low-voltage systems.

Together, these factors point to a market shaped less by broad-based inflation across all material categories and more by concentrated pressure within metals, electrical systems and specialized equipment tied to high-demand sectors.

Several interconnected factors are shaping construction costs entering Q2 2026, including supply chain disruptions, labor availability, energy costs and concentrated demand within specific sectors.

Gordian reports that rising energy and transportation costs are affecting material pricing, particularly among metals and other energy-intensive products. The firm notes that increased fuel and freight costs have added pressure across portions of the supply chain, while uneven manufacturing activity and product availability have contributed to differing cost behavior across material categories.[1]

Procurement analysis from STO Building Group identifies electrical and mechanical equipment as some of the most affected categories entering Q2 2026. In its latest procurement market update, STO reports that lead times for major electrical equipment such as switchgear and large power transformers are still significantly extended, with some large power transformers requiring well over two years for delivery. The report also points to elevated freight costs and broader supply chain pressure affecting electrical, HVAC and other freight-sensitive products.

Growth in data center construction is also affecting material pricing and labor availability in several regions. Robins & Morton reports that healthcare and technology-focused projects are increasingly competing with data center developments for specialized labor and materials tied to mechanical, electrical, plumbing and low-voltage systems. According to Tom Thibeaux, Preconstruction Division Manager at Robins & Morton, some highly specialized trades — including electricians, HVAC technicians and plumbers — are experiencing notable regional labor pressure tied to large-scale project activity.

Broader industry indicators appear to support these trends. Associated Builders and Contractors Chief Economist Anirban Basu has reported continued strength in contractor backlog tied to data center construction activity, while Associated General Contractors of America Chief Economist Ken Simonson recently noted that rising fuel costs are affecting construction input prices and freight-sensitive materials.

Labor conditions remain another important contributor to total installed cost escalation. Gordian also points to labor market data showing lower-than-normal levels of layoffs and voluntary quits within the construction sector.[2] At the same time, firms continue to report wage pressure tied to regional project concentration and competition for specialized workers.

While many of these pressures have persisted in some form since the pandemic-era supply chain disruptions, contractors and suppliers say construction costs entering mid-2026 are being shaped increasingly by concentrated demand within high-growth sectors, evolving trade conditions and ongoing supply chain uncertainty.

As pricing variability and lead-time disruptions persist across multiple material categories, contractors and project teams are placing greater emphasis on early procurement planning and proactive risk management strategies.

According to Hamilton and Allen of STO Building Group, some of the largest procurement challenges entering Q2 2026 involve long-lead electrical and mechanical equipment, including switchgear, transformers, generators and large HVAC systems. In its latest procurement market update, STO notes that extended manufacturing timelines and freight-related pressures are still influencing project scheduling and procurement planning across multiple sectors.

To address these conditions, many firms are accelerating procurement schedules and securing major equipment packages earlier in the design process. STO reports that some project teams are locking in factory production slots before design completion in an effort to reduce schedule exposure and limit the impact of future pricing increases. The firm also notes increasing use of multi-source procurement strategies, domestic sourcing options and aggregated purchasing approaches to improve supply chain flexibility and material availability.

Robins & Morton reports using similar approaches across healthcare and technology-focused projects. According to Thibeaux, project teams are closely monitoring pricing trends and evaluating opportunities for early-release packages, advance equipment purchases and alternative material selections when schedule or budget concerns arise.

Subcontractor capacity and financial stability are also receiving increased attention. STO notes that material escalation, freight surcharges and margin pressure are placing additional

strain on portions of the subcontractor market, particularly among trades with significant exposure to copper, aluminum, polymers and other volatile inputs. As a result, some contractors are placing greater emphasis on procurement structures that reduce disruption associated with material volatility and procurement delays.

Contract language and escalation planning are also evolving in response to market uncertainty. STO reports that contract provisions tied to tariffs and material escalation are becoming increasingly common in commercial agreements as owners, contractors and suppliers seek greater protection against material pricing and delivery uncertainty.

While many contractors report that adapting to changing market activity has become a routine part of project delivery in recent years, firms in multiple sectors report that proactive procurement planning, supplier coordination and early decision-making remain among the most effective tools for managing schedule and cost risk in an uneven pricing environment.

Although national material trends continue to influence the broader construction market, contractors and suppliers report that regional labor dynamics and sector-specific demand are increasingly shaping procurement strategies and project costs at the local level. Gordian reports that some regional pricing differences are beginning to emerge, with material escalation in portions of the Midwest and South occurring at a slower pace than in parts of the Northeast and West Coast. Gordian notes that construction employment growth in several Southern and Midwestern metropolitan areas has remained strong, coinciding with continued project growth across manufacturing, infrastructure, healthcare and technology sectors.[3]

Data center construction activity remains one of the most significant drivers affecting both labor and materials in certain markets. Associated Builders and Contractors’ Basu has reported that contractors working in the data center sector continue to maintain longer backlog levels than many other segments of the construction market.

Both STO Building Group and Robins & Morton point to healthcare, data center and advanced manufacturing activity as areas experiencing increased procurement and supply chain pressure tied to specialized materials and labor availability. STO notes continued strain on electrical and HVAC procurement driven by large-scale project activity, while Robins & Morton reports increasing competition for mechanical, electrical, plumbing and low-voltage systems associated with healthcare and data center development.

According to Thibeaux from Robins & Morton, some of the strongest labor pressures are occurring within highly specialized trades, including electricians, HVAC technicians and plumbers. Robins & Morton notes that these pressures can vary significantly depending on the concentration and timing of large-scale projects within specific geographic markets.

Contractors also report that regional supply conditions and supplier availability do not always align neatly with broader national indicators. Robins & Morton notes that real-time pricing fluctuations are often tied to localized supplier and fabrication capacity, particularly in markets experiencing concentrated demand.

Current market activity indicates that project type, labor specialization and procurement timing are continuing to shape construction costs alongside broader national pricing trends.

Industry participants continue to describe the near-term construction cost outlook as uneven, with most expecting ongoing variation in materials, labor availability and procurement conditions through the remainder of 2026.

Gordian notes that many contractors and project teams report growing uncertainty surrounding long-range pricing forecasts and procurement planning, particularly as energy costs, transportation conditions, tariff policies and global trade disruptions continue to evolve. While some material categories have stabilized compared to the sharp volatility experienced in recent years, metals, electrical systems and other freight-sensitive products are still experiencing upward pressure tied to manufacturing activity, sector demand and procurement timing.

Both STO Building Group and Robins & Morton report that electrical and mechanical systems remain among the most closely monitored categories entering the second half of the year. STO notes that lead times for major electrical infrastructure and HVAC equipment remain extended in several sectors, while Robins & Morton reports continued pressure tied to healthcare, data center and technology-related construction activity.

Copper, steel and fuel- and petroleum-related products are likely to be key areas to watch in the coming quarters due to strong demand, freight exposure and broader uncertainty surrounding global supply conditions. Contractors are also closely monitoring labor availability within highly specialized trades, particularly in regions experiencing concentrated growth tied to large-scale infrastructure, healthcare and technology projects.

At the same time, many firms report that adapting to shifting market conditions has become a standard part of project planning and procurement. Early procurement, supplier diversification, escalation planning and alternative material evaluations are playing a larger role in project delivery strategies as contractors seek to manage schedule and budget risk in an environment shaped by uneven cost movement rather than broad-based escalation affecting all material categories.

While the construction market entering mid-2026 continues to see activity in several major sectors, pricing trends are still expected to vary significantly by material category, region and project type.

Electrical Infrastructure Demand Reshapes Construction Planning

According to Gordian and industry professionals contributing to this report, electrical systems and related infrastructure remain among the most closely monitored areas of the construction market entering the second half of 2026.

Growth associated with data centers, healthcare facilities, infrastructure projects and advanced manufacturing is affecting both procurement timelines and labor availability tied to electrical and mechanical systems in several regions. Switchgear, transformers and other electrical equipment continue to experience extended lead times, while copper wire and conduit recorded some of the strongest increases among tracked material

categories entering Q2 2026.

Copper wire and conduit reflect broader pressure affecting electrical systems and related supply chains. Contractors are also seeing increased competition for skilled trades supporting electrical and mechanical systems, particularly electricians, HVAC technicians and low-voltage specialists.

Regional concentration of large-scale projects is creating differing conditions depending on the timing and scale of major developments within specific markets. Large healthcare,

technology and infrastructure projects can place disproportionate strain on electrical systems, specialized labor and related materials, even when broader construction pricing trends appear more stable.

Gordian notes that many traditional construction materials have shown signs of stabilization compared to the volatility experienced in recent years. However, electrical infrastructure and related systems are expected to remain key areas of focus as contractors navigate shifting demand, specialized labor constraints and extended equipment lead times.

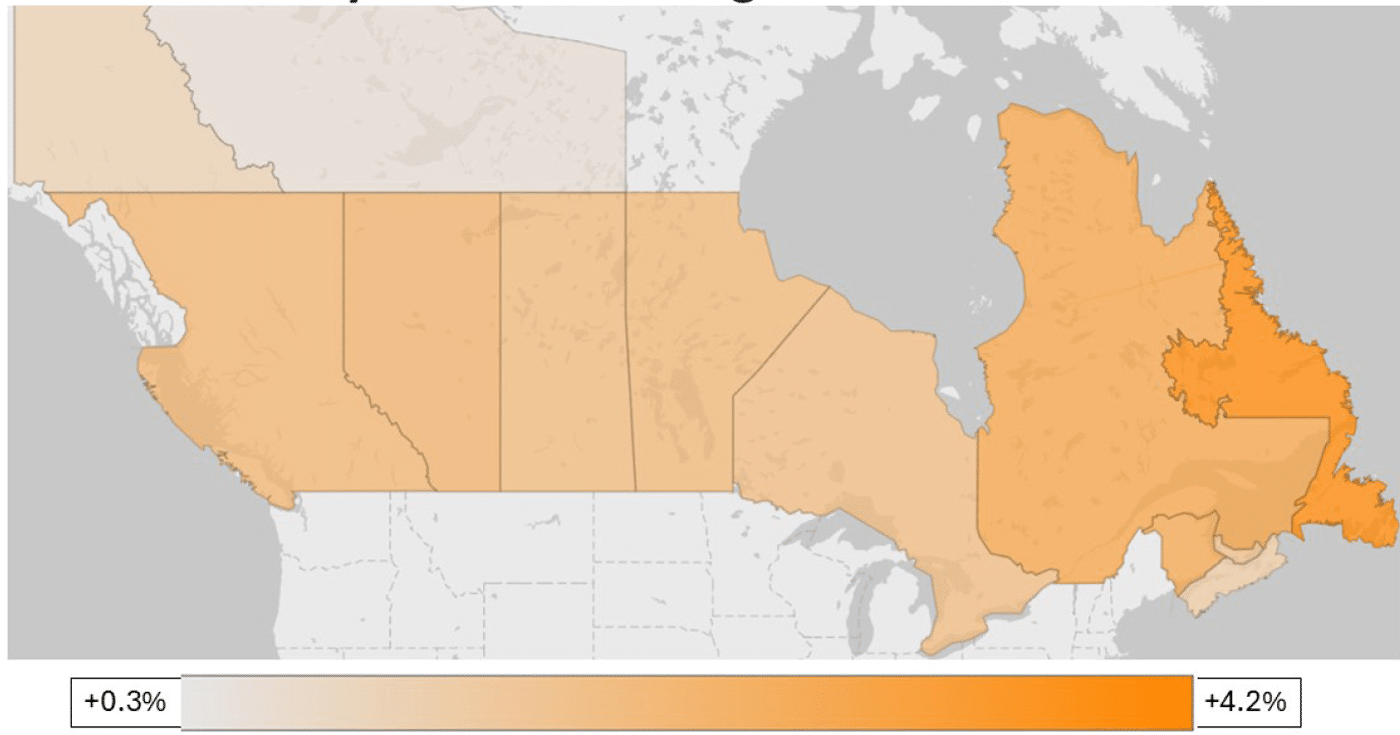

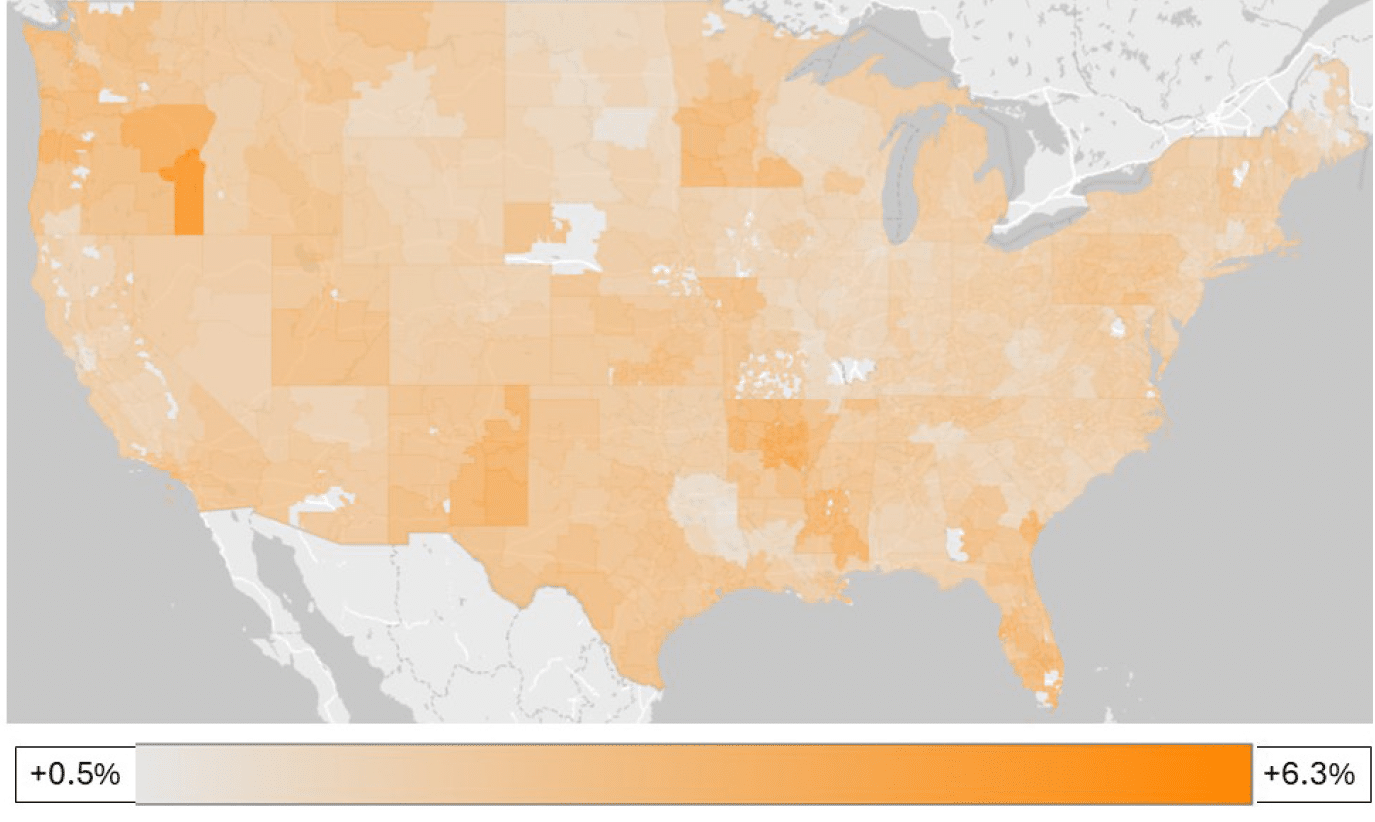

Q1 2026 to Q2 2026

For the first time in the history of this report, quarterly costs in the United States only rose. The increases were mostly moderate, as low as 0.5% in some regions, but let’s not bury the lede: It is a significant development that construction costs rose across America.

Further, it is surprising that these conditions were mirrored across Canada. While the increase range was more compressed in Canada than the U.S., the upward movement is still steep enough to pinch.

Certainly, neither of these cost developments can be divorced from the massive spike in fuel and energy costs. As long as those costs remain elevated, it is likely that this pattern will continue.

CANADA

USA

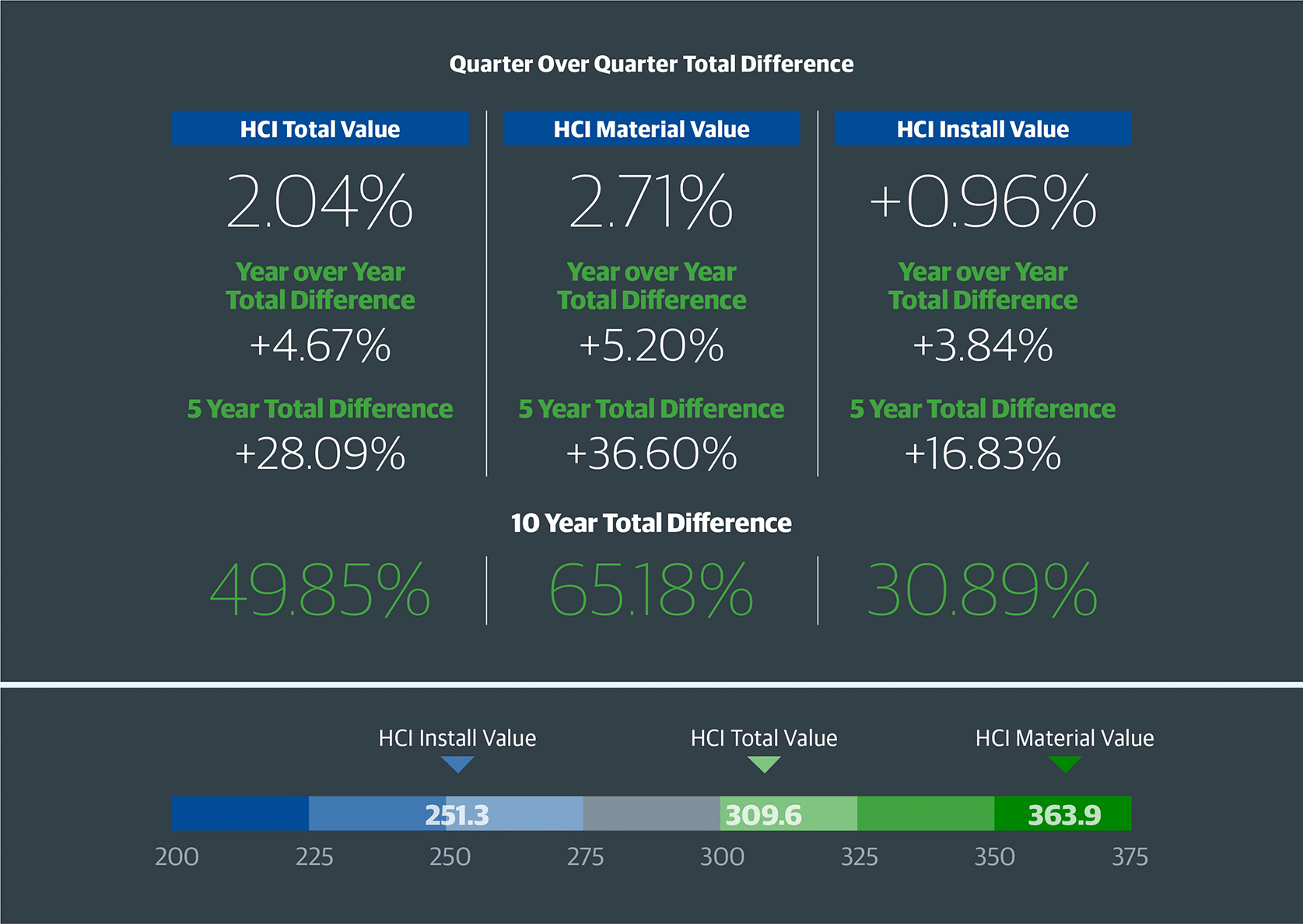

The HCI (Historical Cost Index) is an invaluable tool to track changes in the cost of construction materials and labor over time. The HCI Total Index Value represents the overall change in construction costs, including materials, labor and installation expenses. The HCI Material Value tracks the change in the cost of raw materials, such as lumber and steel. The HCI Install Value measures the change in the cost of installation labor, including plumbing, electrical and HVAC. These indices provide valuable insights, helping building industry professionals to anticipate and plan for changes in construction costs and make informed decisions about project budgets and timelines.

NOTES:

- The index values are based on a 30-city national average with a base of 100 on January 1, 1993. The three numbers are the total, material and install index numbers, respectively, for the 30-city national average in 2026.

- The Historical Cost Index (HCI) applies the quarterly City Cost Index (CCI) updates to a historical benchmark and allows specific locations to be indexed over time. These indexes with RSMeans Data are a vital tool for forecasting construction costs and can be a valuable source of information for comparing, updating and forecasting construction costs throughout the United States.

What the data says:

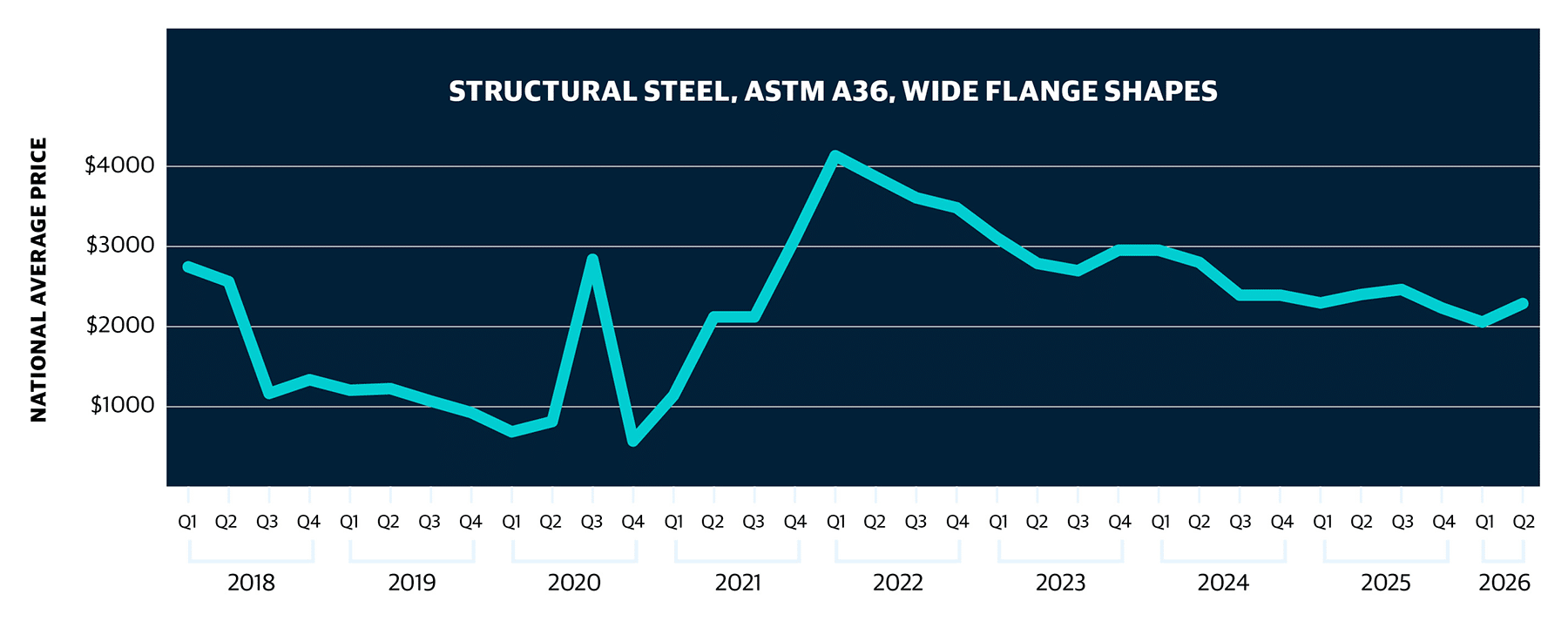

- Structural steel costs increased 7.50% quarter over quarter in Q2 2026 but remained 3.27% below year-ago levels.

- Structural steel pricing showed renewed upward movement during the quarter following softer year-over-year comparisons earlier in the year.

View from the field:

Structural steel costs moved sharply upward entering Q2 2026 as energy-related manufacturing costs and tariff activity intensified across portions of the metals market.

GORDIAN: “The increase in costs appears to be tied to tariffs and energy costs associated with manufacturing.”

STO BUILDING GROUP: “Steel pricing remains vulnerable to tariff activity, domestic mill capacity constraints and broader energy-related cost pressures.”

Material Description: Structural steel, ASTM A36, wide flange shapes, two-story office building, beams and columns, field bolting.

Measurement relative to this data: National average cost is per ton of structural steel, ASTM A36.

Read more on what the data says about steel.

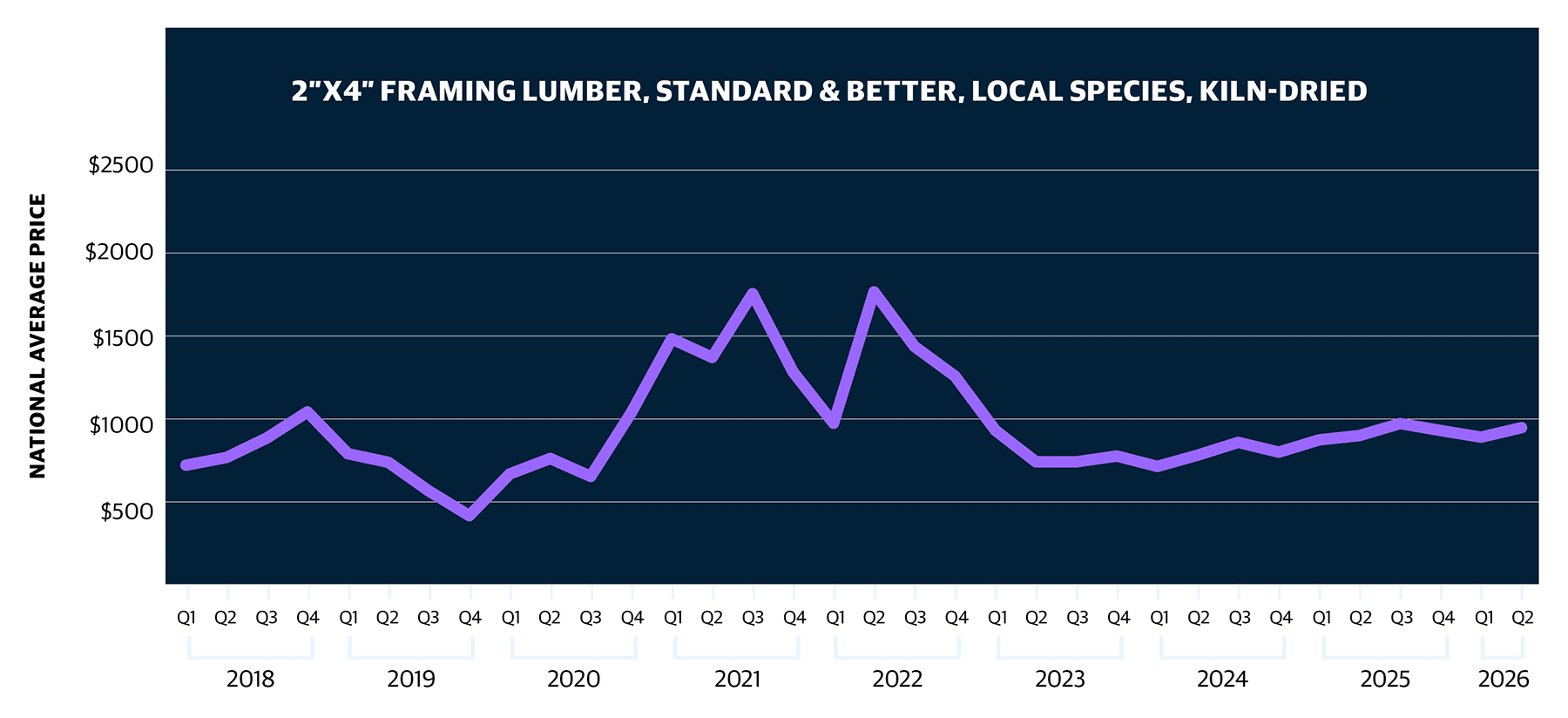

What the data says:

- Framing lumber costs increased 5.11% quarter over quarter and 4.21% year over year in Q2 2026.

View from the field:

Framing lumber costs increased at a more moderate pace than many metals and electrical products during the quarter, with contractors reporting steadier procurement conditions than in several other material categories.

GORDIAN: “While costs could continue to rise in the near term, increases are expected to remain in the single-digit range.”

ROBINS & MORTON: “Wood framing materials have been more manageable from a procurement standpoint compared to electrical and mechanical systems.”

Material Description: 2” x 4” framing lumber, standard & better, local species, Kiln-dried.

Measurement relative to this data: National average cost is per square foot of the material costs. National average cost noted is per MBF (thousand board feet) of 2” x 4” framing lumber.

Read more on what the data says about lumber.

What the data says:

- Concrete block costs decreased 0.82% quarter over quarter but remained 1.67% above Q2 2025 levels.

View from the field:

Concrete block remained one of the more stable material categories compared to many metal-based and freight-sensitive products.

GORDIAN: “Concrete block pricing has remained more stable than related products such as ready-mix concrete.”

ROBINS & MORTON: “Several suppliers have indicated that additional concrete and masonry-related increases may occur later in the year.”

Material Description: Concrete block, reg. weight, hollow, ASTM C90, 8” x 8” x 16”, 2000 psi (pounds per square inch).

Measurement relative to this data: National average cost is per square foot of the material costs. National average cost noted is per one block of concrete, ASTM C90.

Read more on what the data says about concrete block.

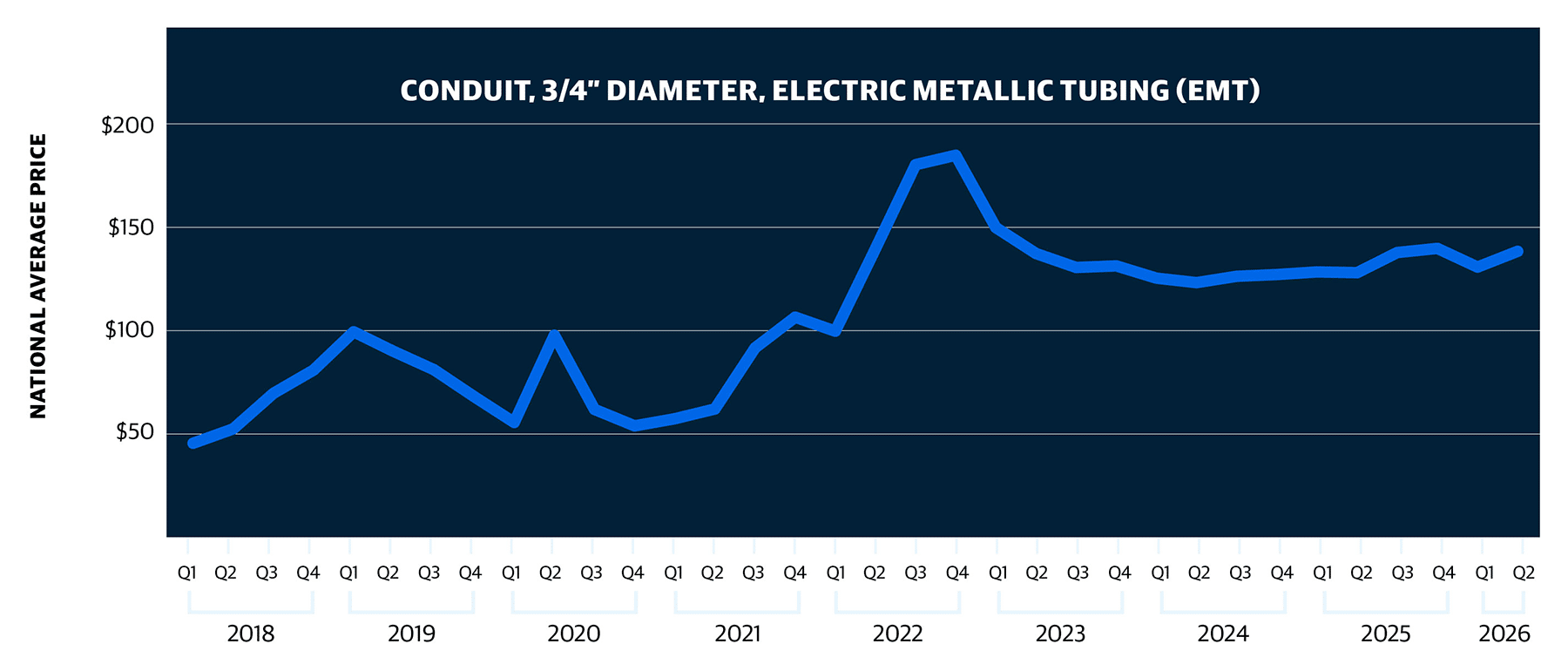

What the data says:

- Conduit costs increased 5.22% quarter over quarter and 7.20% year over year in Q2 2026.

View from the field:

Conduit pricing increased during the quarter alongside broader escalation across electrical and metal-based products.

STO BUILDING GROUP: “Extended lead times for electrical infrastructure and related equipment continue to affect procurement planning across multiple sectors.”

Material Description: Conduit, 3/4” diameter, electric metallic tubing (EMT).

Measurement relative to this data: National average cost is per square foot of the material costs. National average cost noted is per CLF (hundred linear feet) of EMT (electric metallic tube) conduit.

Read more on what the data says about conduit.

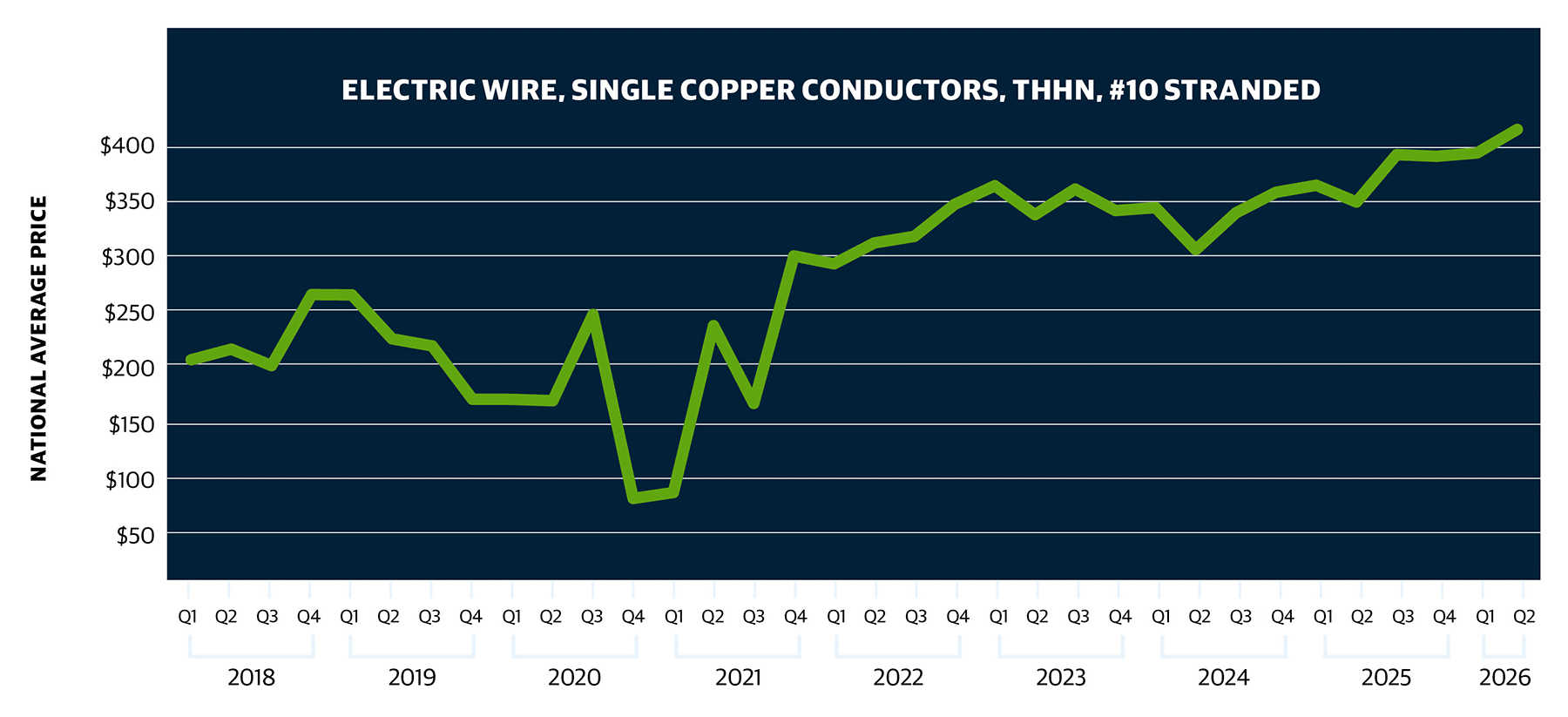

What the data says:

- Copper electric wire costs increased 5.30% quarter over quarter and 18.42% year over year, representing one of the strongest annual increases among tracked materials.

- Copper-related materials continued to show strong upward movement entering Q2 2026.

View from the field:

Copper-related materials saw some of the sharpest cost increases entering Q2 2026, driven by supply constraints and strong demand tied to electrical infrastructure and large-scale technology projects.

GORDIAN: “Copper-related materials continue to experience some of the strongest year-over-year increases among tracked categories.”

ROBINS & MORTON: “Competition with data center construction is continuing to affect pricing and availability across mechanical, electrical, plumbing and low-voltage systems.”

STO BUILDING GROUP: “Copper markets are experiencing the largest supply deficit seen since 2004.”

Material Description: Electric wire, single copper conductors, THHN, #10 stranded.

Measurement relative to this data: National average cost is per square foot of the material costs. National average cost noted is per MLF (thousand linear feet) of copper wire.

Read more on what the data says about copper electric wire.

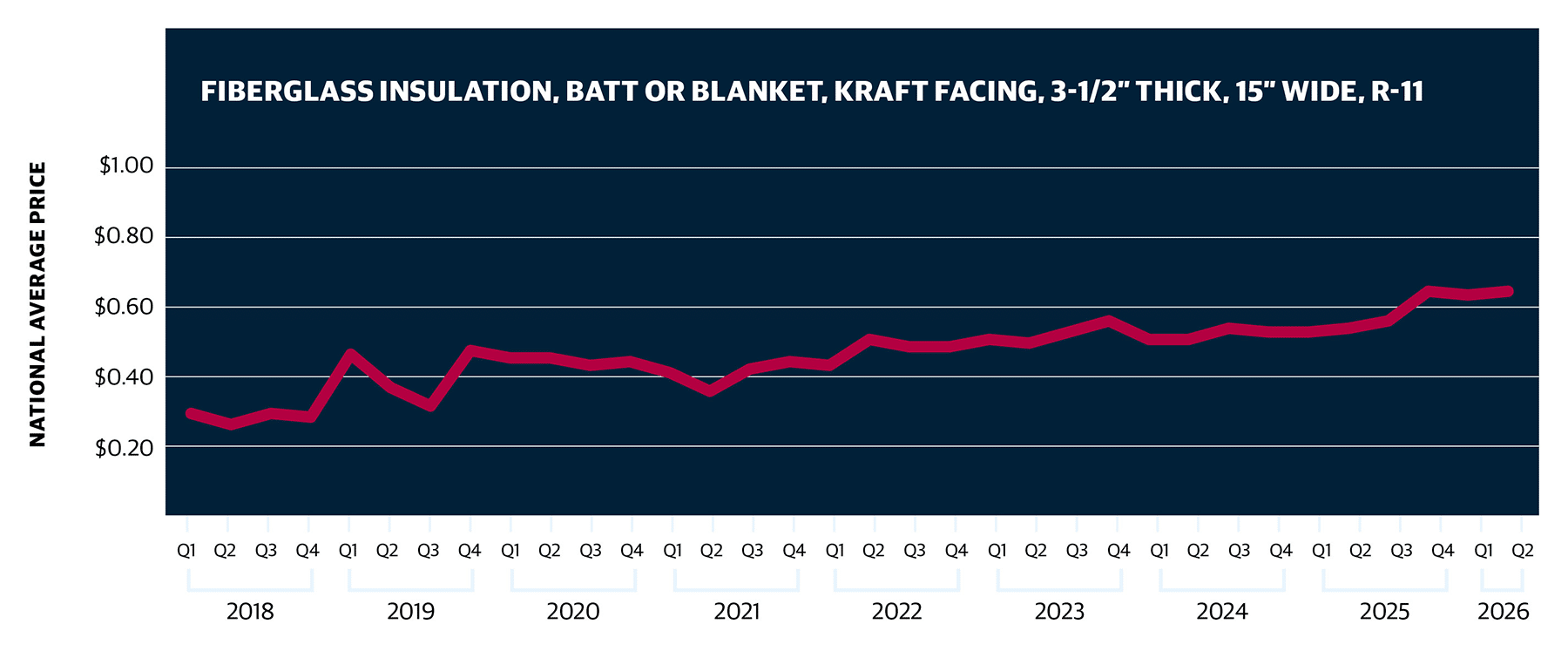

What the data says:

- Fiberglass insulation costs increased 1.26% quarter over quarter and 18.49% year over year in Q2 2026.

- Fiberglass insulation pricing remained comparatively stable during the quarter despite elevated year-over-year comparisons.

View from the field:

Fiberglass insulation pricing showed relatively limited movement during the quarter, though freight and transportation costs remain an area of concern for contractors.

GORDIAN: “Insulation pricing has remained relatively stable in recent months.”

STO BUILDING GROUP: “Freight-sensitive materials continue to experience uneven pricing conditions tied to transportation and supply chain pressures.”

Material Description: Fiberglass insulation, batt or blanket, Kraft facing, 3-1/2” thick, 15” wide, R-11.

Measurement relative to this data: National average cost is per square foot of the material costs. National average cost noted is per square foot of fiberglass insulation.

Read more on what the data says about fiberglass insulation.

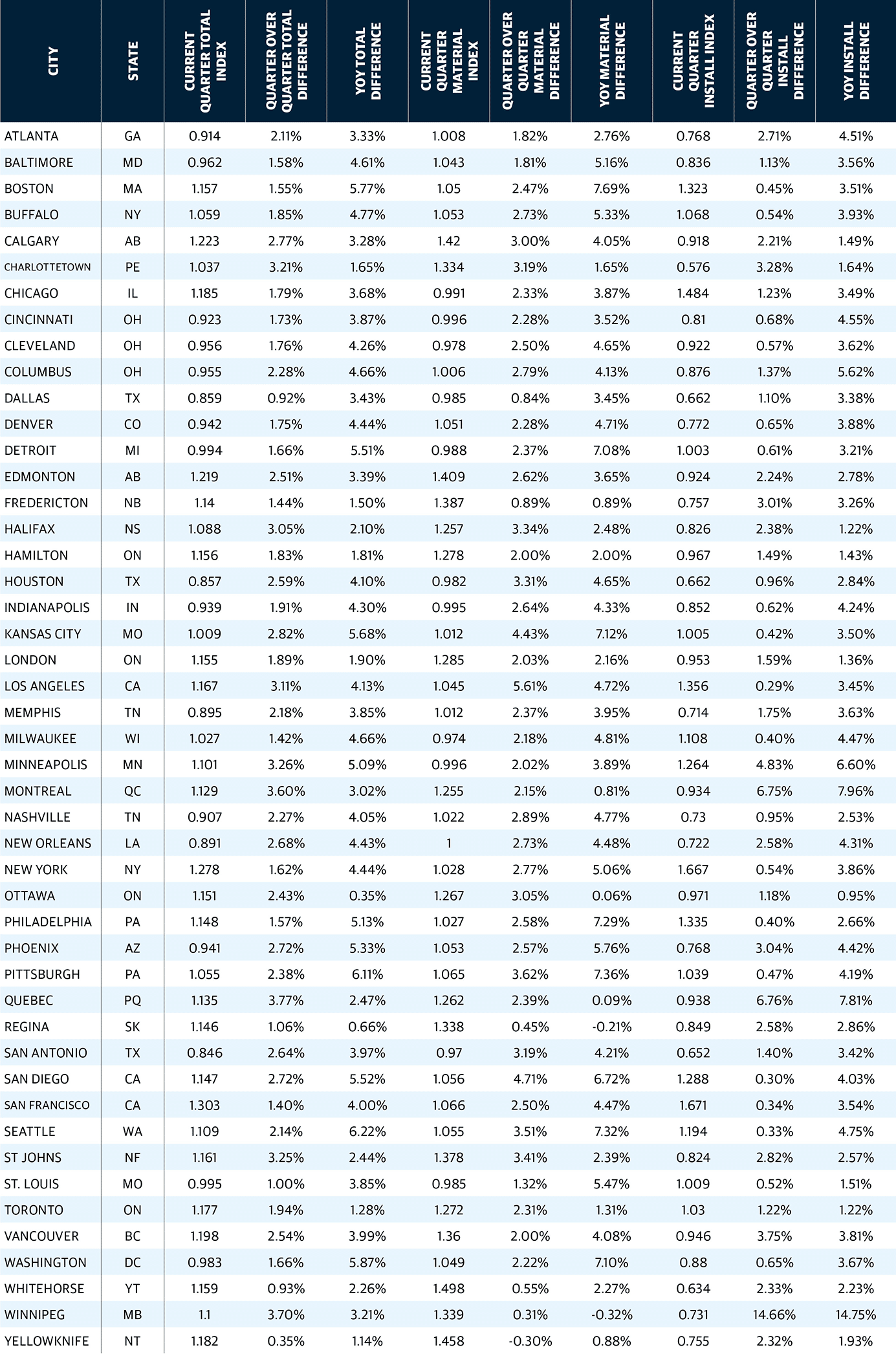

The City Cost Index is a quarterly data product designed to answer the question, “How much higher/lower are costs in my city relative to the national average?” The CCI can be used to better reflect localized pricing in construction estimates. Each quarter, Gordian’s RSMeans™ Data research team collects prices from cities across the United States and Canada, which are then compared to the national average and the current year’s annual release data to create the CCI. The City Cost Index shows a factor for Material, Installation and Total with rows representing multiple CCI divisions. Additionally, the CCI shows a Material Total, Installation Total and a Total Weighted Average.

- Gordian Construction Data and Insights Hub

- Associated Builders and Contractors. “Construction Backlog, Contractor Confidence Outpace Year-Ago Levels in March.” ABC News Release.

- Associated General Contractors of America. “Construction Materials Costs Climb In March, Driven By Near-record Jump In Diesel Fuel Price And Further Increases In Prices For Key Metals.” AGC News Release

- Allen, Doug, and David Hamilton. Procurement Market Update: Shifting Market Dynamics. STO Building Group, Q1 2026.

- [1] “California’s oil and jet fuel supply is getting slammed by a

perfect storm of unfortunate timing — and help is years away.” Fortune - [2] JOLTS Home. U.S. Bureau of Labor Statistics

- [3] State and Area Employment. U.S. Bureau of Labor Statistics.

The Following Supply Chain, Preconstruction and Sustainability Subject Matter Experts Contributed their Views for this Q2 2026 Analysis:

Gordian

Adam Raimond, Program Manager, Construction Indices

Robins & Morton

Tom Thibeaux, Preconstruction Division Manager

STO Building Group

David Hamilton, Senior Vice President, Construction Procurement Solutions

Doug Allen, Manager, Strategic Growth & Corporate Development

Share this:

in 2026 2")