The State of Facilities in Higher Education, 12th Edition

Executive Summary

The past several years this report has been written amidst a pandemic and its aftermath, as well as the impending enrollment cliff. It could not seem to separate itself from complicated issues driving existential commentary. The 12th annual State of Facilities in Higher Education arrives as we sit on the precipice of the cliff, a complex social mood toward higher education that challenges enrollment further and our federal government reimagining education nationally — adding further uncertainty.

With that backdrop, we continue to monitor key trends, including:

- An ongoing curtailment of campus expansions as schools take stock of what they will really need to own and operate.

- Sustained shortfalls in funding campus renewal investments of more than 32%.

- A backlog of capital renewal needs which has grown at a more modest 2% this year, is once again this year over $140/gsf.

- Operational spending keeping pace with inflation, but not yet recovered from reductions that happened before and during the pandemic.

This year we also spend some time exploring artificial intelligence which seems to be all around us. AI is appearing more slowly in facilities organizations as it is less clear how to best leverage it operationally or make the time/resources available to do so given ongoing financial limits.

Since Professor Nathan Grawe raised the specter of the enrollment cliff in 2018 in his book, “Demographics and the Demand for Higher Education,” the higher education community has been anticipating its arrival. There was uplifting news in the short term in January 2025 when the National Student Clearinghouse Research Center updated earlier pessimistic data to report student enrollment jumped a stunning 4.5% in the fall. It is not at all clear yet if this trend somehow represents a challenge to the broader demographic indicators or a final surge before the cliff.

We continue to watch along with others in higher education for signs that there will be an expansion in the industry. While hopeful that every institution will find its way forward, our data once again indicates that campus facilities will remain a tremendous drag on any school not financially prepared for what we called in 2017 the “inevitable entropic demands of buildings and their systems.” They age and we can’t prevent it. Schools can only respond with reinvestment, replacement, building failure or institutional closure.

Act or be acted upon; it is with this call that we explore some familiar metrics and new technologies.

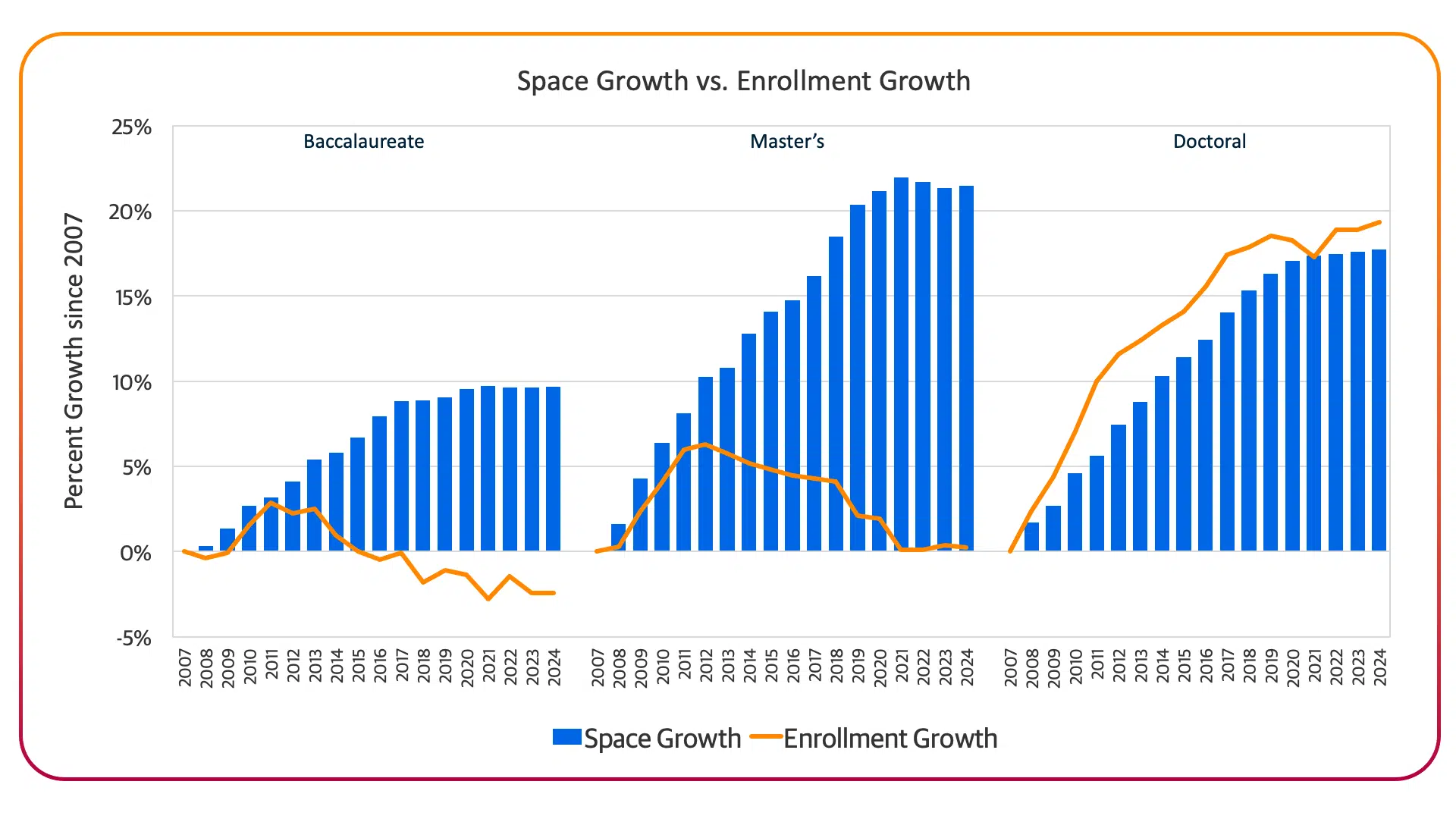

There are some schools (27% of our database) that are seeing continuing signs of expansion, though that growth is a relatively modest 3%. Some continue because they are not yet feeling the pressure financially to keep up with what they have already built. And others sustain because they are indeed still adding students. Still, the largest majority of institutions have settled into a multi-year curtailment in expansion. Construction continues and advancements in the quality of buildings that students are using to pursue their education are improving but often while replacing older structures which needed to be removed. It is important to note that these enhancements are being implemented with more thought to the costs to sustain that investment and healthy caution about a future with great uncertainty.

With 2025 upon us, we have arrived on the cusp of the much discussed enrollment cliff. In parallel we have also now experienced about a half a decade of skepticism about the value of higher education to individuals and society, driven by cost and cultural questions. This combination makes the view forward for students a bit messy and predicting what will happen across both the industry and for individual schools equally fuzzy.

The impacts of the cliff on the overall pool of students available to fuel the higher education community are all but guaranteed. With birthrates dropping since 2008, the number of 18-year-old citizens available to attend a collegiate experience has been tracked nearly their whole lives. The Western Interstate Commission for Higher Education (WICHE) is now forecasting that this birthrate decline will yield a 13% decrease in high school graduates from 2025 through 2041. A steady decline in international students since the mid 2010s does not present an option to fill the enrollment gap either. The total pool of students won’t shrink enough to impact the most selective and sought-after schools where enrollment will stay steady or even continue to grow as students committed to continuing their education will seek stability and value.

But for those institutions that have been struggling, difficult choices that many have been talking about for several years now are upon them. Most sustaining models involve reimagining the institution as a smaller place with reductions in employees and property to align spending with revenue. Alternatives demonstrated over the past decade would include merger, sale or dissolution. Anyone not preparing already for this moment has a steep hill to climb.

The expanding skepticism about the value of a collegiate education will add further to this challenge. Reasons for that skepticism are many. First is that the sticker price of a year of college is now greater than it has ever been, far outpacing the incomes of many and feeding narratives about it being only for those individuals and families of means. The industry is also not doing the best job contradicting that narrative, despite countervailing information indicating that aid programs have actually kept costs neutral or down over the past 20 years.

Beyond the Sticker Shock: College Costs

Based on research by the College Board, it would appear that while total costs for higher education continues to rise, net tuition and fees in fact dropped or stayed stable over the past 20 years. That research is explained in more detail by the Bipartisan Policy Center and can be found here

While that is encouraging news for students and families, it provides one more reason why free dollars to address campus facilities needs remain so difficult to release.

Questions about the social impact of a collegiate community on individual students has stimulated the rise of new and different kinds of universities, moves to remake how universities are run and led and even some social messaging that suggests turning away from higher education altogether. While this will all shake out over the long term in an industry that will be remade in some fashion, it is coming at a difficult time in the short term for institutions that are tuition driven and rely on a steady stream of students to operate.

And finally, 2025 has opened with the federal government actively reimagining its role in education at all levels, which may further shuffle the financial tools that schools use to deliver programs and make them affordable. The government is also reevaluating the investments it makes in schools to do research, which could have a deep impact on the top tier institutions across the country that provide fundamental research in science, medicine, the humanities and more.

It is a complicated and, as noted earlier, messy time to operate a college or university. Having the best possible information about an institution’s particular situation as well as the larger context will be essential in leading the way forward.

Space

Conversations about space utilization continue to occur on campuses, just as they continue across the real estate sector.

While housing stock across the United States is at a premium nearly everywhere, even in locales where the population has experienced a slow down or decline, retail and commercial spaces are much more readily available. Movements have arisen to send people back to the office, but those efforts have not yet turned the tide on hybrid or remote office practices, cutting a seemingly unalterable swath through office space occupancies. That reality continues to be revealed in a leveling off of space creation on campuses across our database.

There are some schools (27% of our database) that are seeing continuing signs of expansion, though that growth is a relatively modest 3%. Some continue because they are not yet feeling the pressure financially to keep up with what they have already built. And others sustain because they are indeed still adding students. Still, the largest majority of institutions have settled into a multi-year curtailment in expansion. Construction continues and advancements in the quality of buildings that students are using to pursue their education are improving but often while replacing older structures which needed to be removed. It is important to note that these enhancements are being implemented with more thought to the costs to sustain that investment and healthy caution about a future with great uncertainty.

Carnegie Classification System Update

The Carnegie Classification System, which has been segmenting our database and comparative materials into objective, degree-based categories, is undergoing significant updates in the spring of 2025. While this year’s State of Facilities will continue to rely on the historical framework, we believe it is essential to continue to acknowledge the evolving shift. The new classification system will create more subtlety and granularity for exploring institutional groupings. The first piece of the update, released in early February, formalizes the introduction of three distinct research classifications – Research 1: Very High Spending and Doctorate Production, Research 2: High Spending and Doctorate Production, and Research Colleges and Universities. These categories expand the understanding of what research can look like in Higher Education, and will act as an overlay on the fundamental four-year institution classifications of Baccalaureate, Master and Doctoral.

The Carnegie Classification System expected updates’ impact on analyses is unclear as of this writing/publication, but we will be incorporating these new classifications into our work as soon as feasible for exploration and trends. To that end, you will observe the first of those changes this year with an edit to graphic images that replaces the singular research designation with a doctoral category. In practice this doesn’t meaningfully alter our historic analysis and lays the groundwork for a more nuanced exploration in future years.

If you have any questions or ideas about how to best utilize the new structure, we welcome your feedback. Please connect with a Gordian team member that you already work with today or reach us at [email protected].

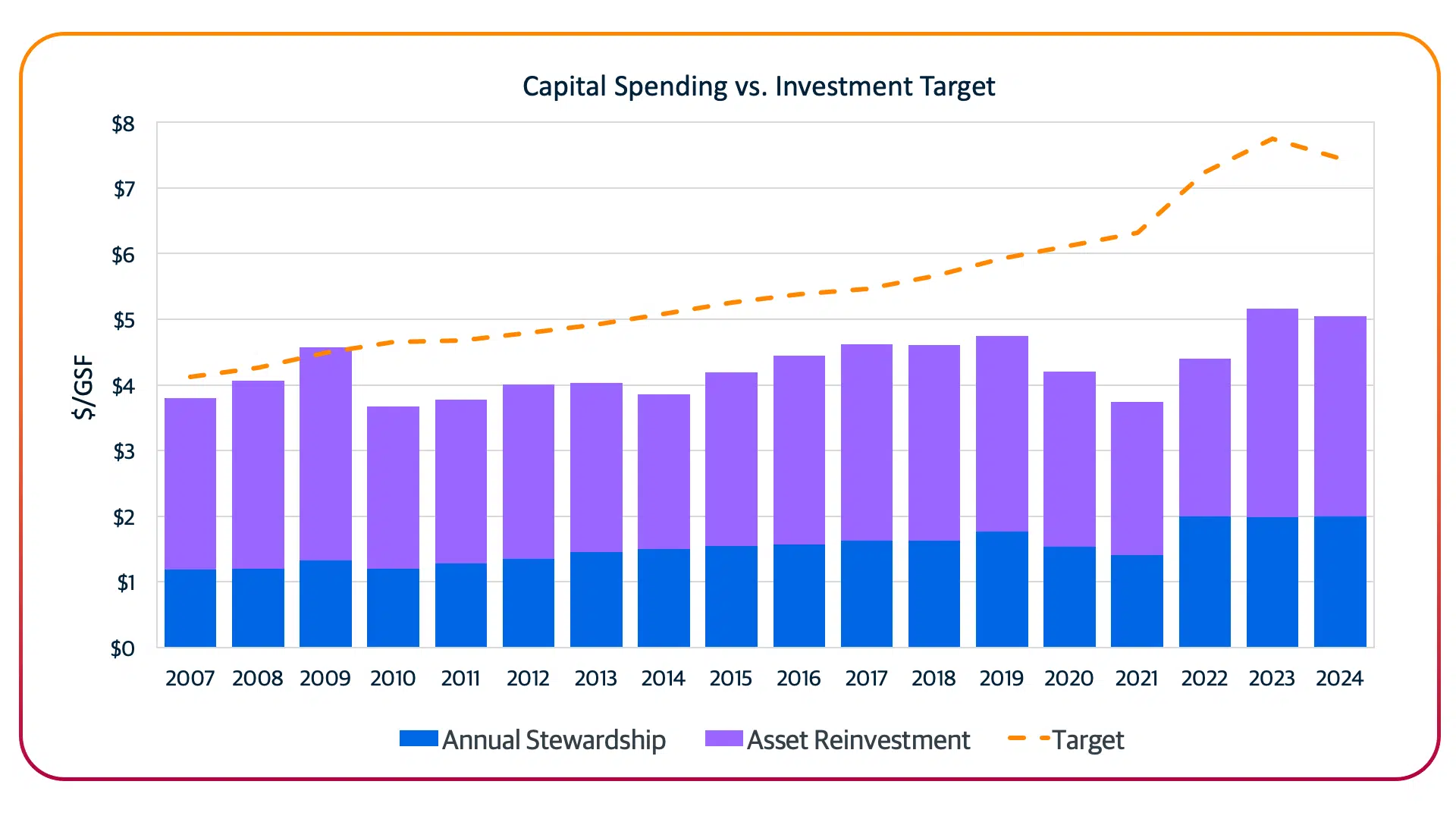

Investment

There has been a rebound in investment in existing campus assets over the past several years. The ever-increasing competition for students demands outstanding faculty and programs. But it also requires a place worthy of the investment that families and individual students are being asked to make. That investment meant a 26% increase in dollars for renovation of existing buildings from 2022 to 2023. Yet marked increases in inflation offset any opportunity to reduce the gap between what is being spent and what is needed.

While inflation tailed off somewhat in 2024, so has spending on campuses, with a slightly improved but still daunting 32.5% funding shortfall. The fact that a large recovery shift has slowed four years after the pandemic is neither surprising nor inherently bad, as it continues to sustain existing investment value. But it unfortunately is not a move that will shrink the gap between what is being invested and what is needed to sustain the institutional assets. Thus, the backlog of need in campus property will continue to grow.

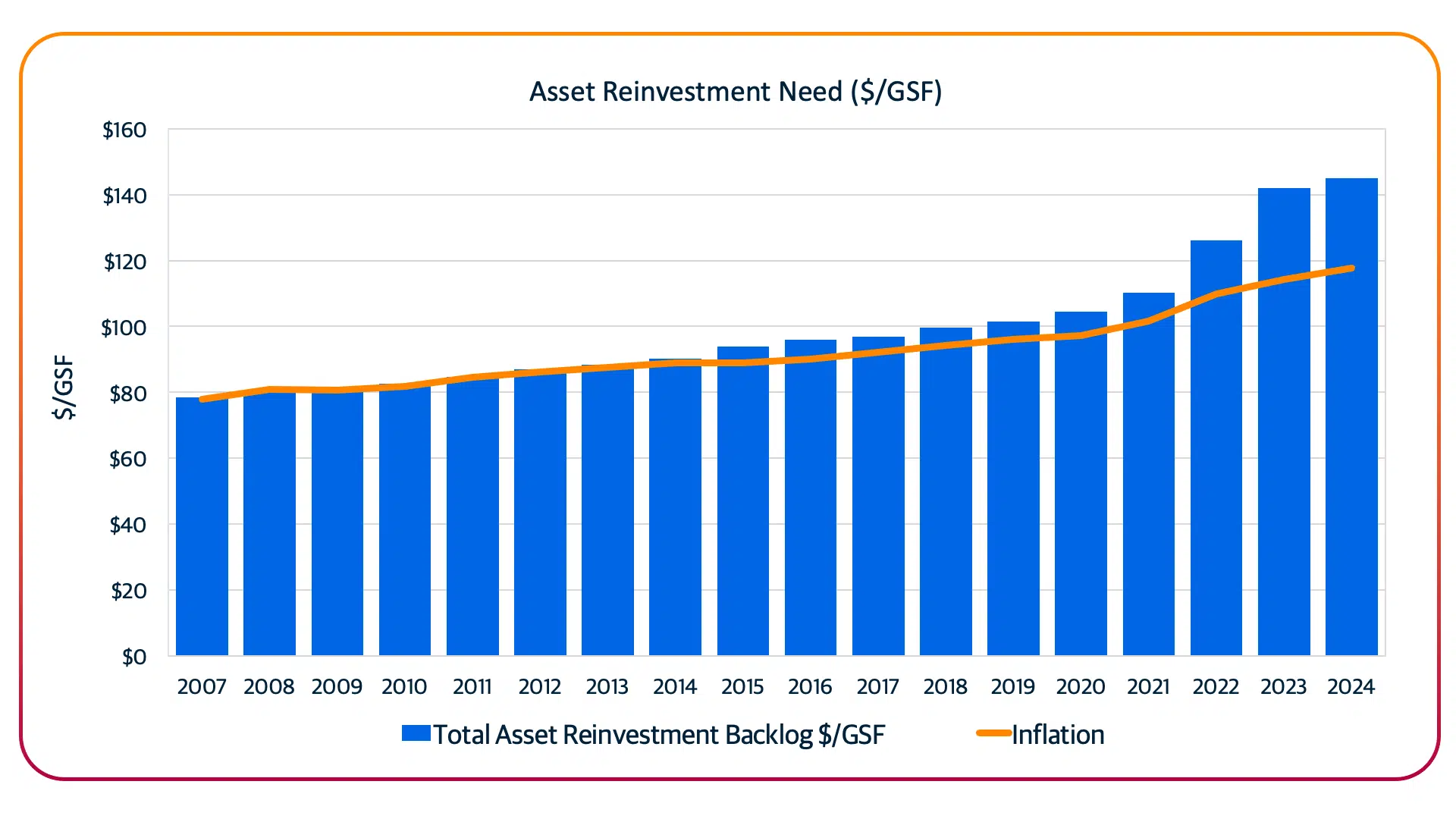

Deferred Capital Renewal

Campus facilities needs can be shaped by the overall age of the building stock, the quality of the initial investment in that property, unique weather and natural disaster events and even the level of care that is provided over time. But the overriding issue continues to be whether sufficient investment is made in a timely manner.

We continue this year with language that recognizes unmet need is rarely the result of a willful postponement of maintenance activity. Maintenance is rarely being deferred by facilities organizations. Most often, a deferral occurs in the investment of the necessary cyclical dollars required as capital assets are reaching their useful life and require renewal dollars to be spent. Capital renewal investment is being deferred. This distinction continues to be important as it recognizes that the responsibility for, and prioritization of, such major investment rests within institutional decision making.

Without those capital renewal dollars, it is not possible for a building to stay in adequate condition. And it is unreasonable to expect buildings will continue to deliver their full capability for the people they serve.

With investment dollars slowing, a continued increase in the backlog of need on campuses is a natural outcome, this year rising only slightly more than 2%. That increase is tempered some by the reduced inflationary pressures. But that combination produces only a reduction in the rate of increase, and not a reduction in the need itself which remains over $140/gsf. On campuses this year, we continue to hear stories of planned project costs outstripping available and allocated budgets, tempering the impact of even the most well-meaning and thoughtfully directed dollars.

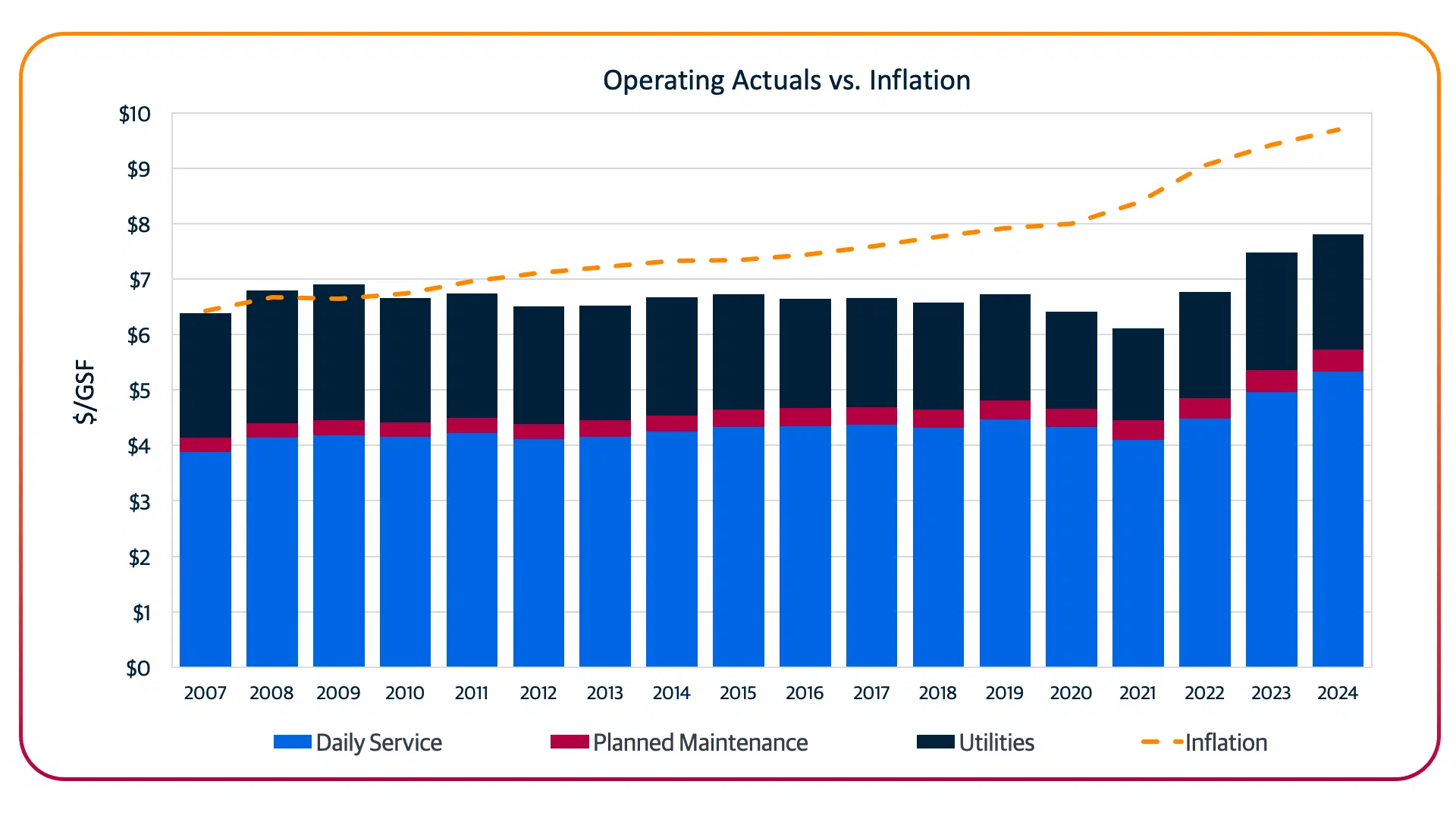

Operating Spend

Annually we are reminded of the importance of adequate operating spending to sustain the functionality and performance of campus spaces. Operating dollars provide for the custodial, grounds and maintenance resources needed to assure building occupants are able to optimally utilize the spaces for the program designated to take place there. Optimal use starts with safe and healthy spaces that function as designed for occupants.

These dollars also make sure that individual assets have the best opportunity to reach their expected useful life and perhaps, as is often the case, beyond that useful life. The story here echoes that from capital renewal in many ways. Spending was up overall about 4.5%, while inflationary pressures raised target need just under 3%.

Spending growth in this area has tempered somewhat. Utility expenditures are down slightly (3.3%) while other expenses are up (about 6.3%). This is a notable drop from the preceding two years when growth in daily services and planned maintenance spend were at 9% (2022) and 10% (2023).

Reasons for a slowdown in facilities operating spending growth at any given campus are unique to that campus. There may not be the capacity, or will, to spend more. There may have been legitimate opportunities to cut back on spending based on innovation, enrollment decline or program changes. But there are usually going to be drivers outside of the department’s immediate control like salaries and wages, utility costs and any number of commodities expenses which continue to drive costs upward. Or institutional decisions to keep key revenue sources like tuition from growing, curtailing the sources for operational spending growth.

It is those uncontrollable drivers which make the gap between need and actual spend so critical. As with capital renewal dollars, underfunding in this area has carry on costs. It can accelerate the degrading of asset condition and, moving forward, the need for replacement. Also, it can create unsafe or unhealthy conditions. And more often than not, it expands the opportunities for performance failures that impact program, from research to athletic performance to simply the quality of rest students get in a residence hall. Each of these has an impact on the student experience and may drive students and faculty to ask why they are committed to the institution.

Staffing

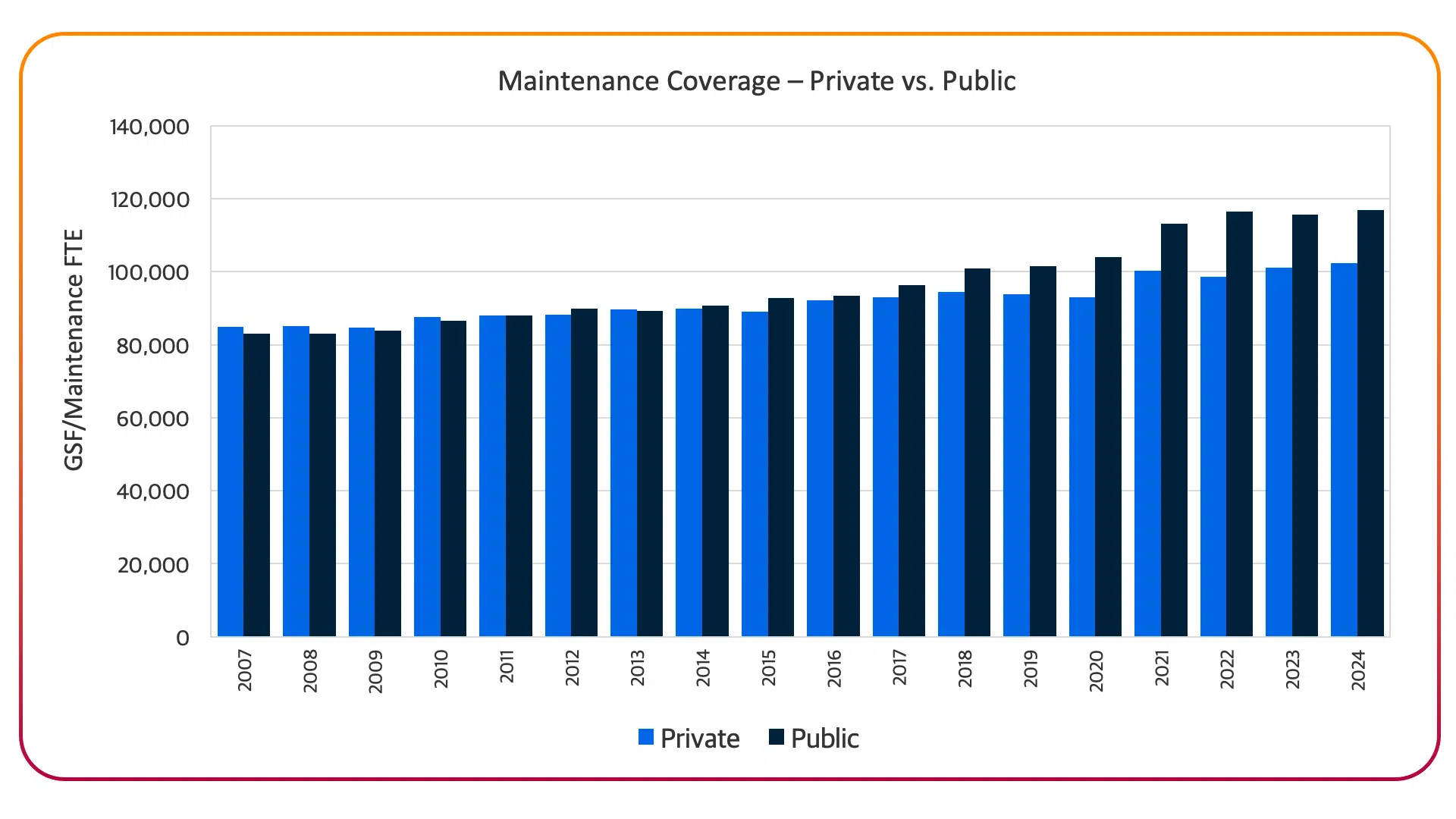

A subset of operational costs is people, which for all colleges and universities is routinely the single largest cost in the budget. The facilities organizations in these institutions also demand significant dollars for people, but it is a markedly smaller share of an organizational budget that also includes allocations for utilities, supplies, specialty contractor/business partners expenditures and often recurring small project dollars. Yet it is the people overseeing those other dollars that control the quality of the spending.

We frequently refer here to maintenance coverage as a key performance indicator of personnel spending. Repeatedly our teams on campuses make clear that these indicators are not absolutes, but rather about the organizational priorities. Last year we spoke directly to the rise in the use of technology to aid in the performance of facilities employees, and that trend has certainly not shifted in the year since. So, it is perhaps not surprising that we do not see any marked trend downward across our database. The amount of space that employees are asked to care for continues to drift slightly upward, with private institutions slowly reducing the gap with their public peers.

Each campus must explore whether these changes are moving the institution toward a point of concern about appearance, performance and/or safety. This requires a careful weighing of a number of local variables to assess whether the impact of this ongoing expansion of responsibility is an empowerment of existing teams or a potential exposure. It is fair to say that broadly in the database this continues to be an area of greater performance pressure, and a likely source of risk. Even where it is intentional, the constraints on resources represent a likely reduction in resiliency or capacity to address unplanned adverse conditions.

Service Levels

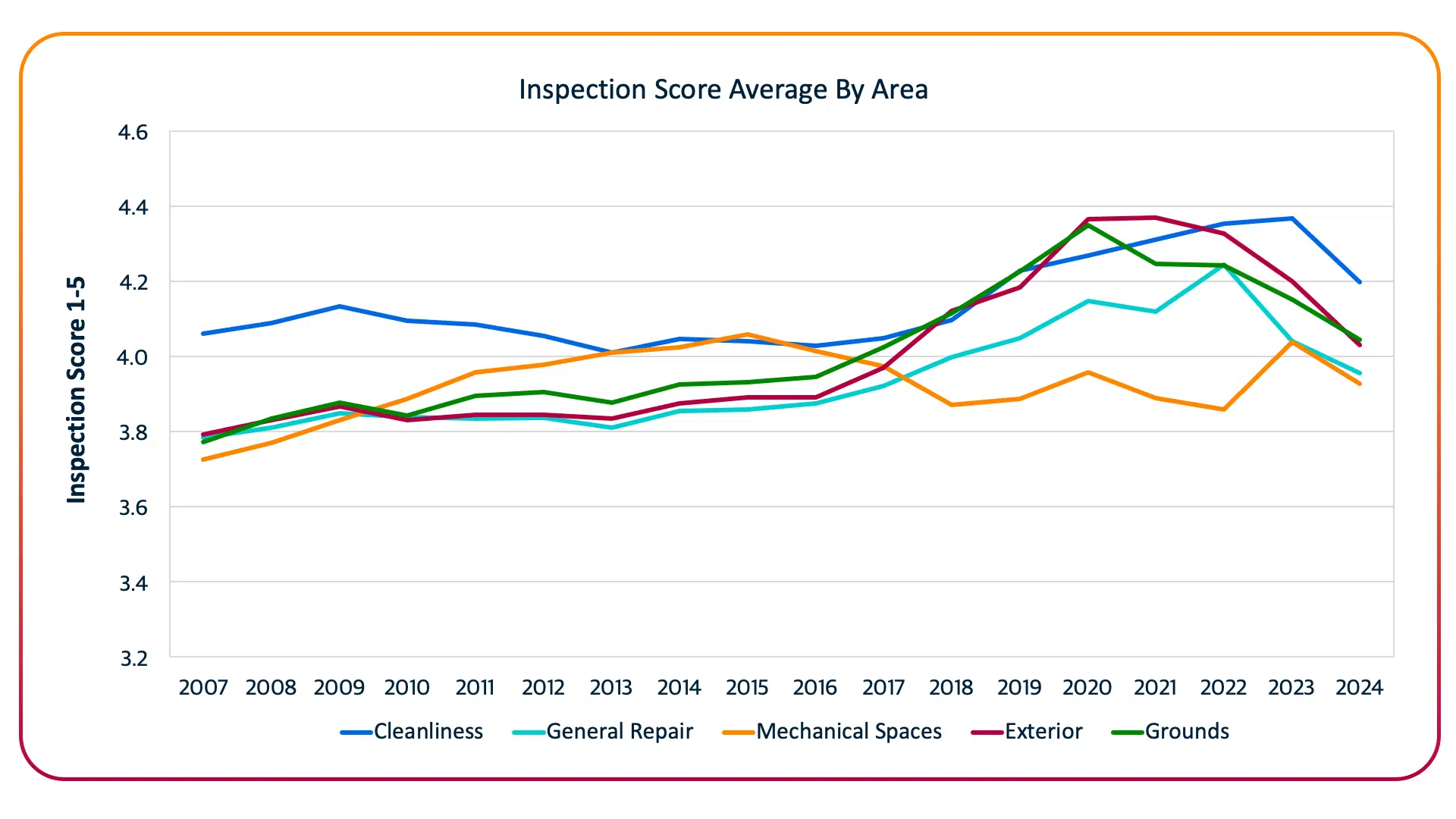

Last year we cautiously introduced a new data point that represented service levels based on local qualitative inspections. We introduced it because we were concerned about a sudden change in the overall conditions in conjunction with the qualitative nature of the data set.

We are able to share this year that our cautious approach was warranted. After more intense scrubbing of the data set, we can report that the previously indicated drop-off was a data issue and not a reflection of campus conditions. We share the update here as a counterpoint to the data from last year and expect to once again drop this measure in future reports. While there is reason to believe that some decline has been happening on campuses most affected by financial stress, it is not happening at the broad scale our data reported previously. And recent reductions keep the data set in roughly the same range it has been for some time.

The call here remains to raise awareness that your institution may be experiencing impacts from the financial challenges you are facing and it would be valuable to take even a qualitative measure of your overall level of care now, so you can be aware of any downward pressures moving forward.

Each year we include a discussion of other emerging influences on campuses. This year, that simply must be a reflection on AI. It would seem the recent arrival of artificial intelligence into our world has few historical parallels with regard to pace and level of impact. Rob Murchison, Co-Founder of Intelligent Buildings, LLC, notes that “AI has been the fastest growing technology ever (ChatGPT reached 100 million individual users two months after its release) because it is so relatable and intuitively valuable.” Unlike machine language which “relies on supervised learning to address issues in complicated data sets” (essentially managing big data), “AI solves complex problems where the decision making is not binary.”

Sure, we’ve been hearing about smart technology for decades — really since the first use of the phrase “artificial intelligence” in 1956. Over the years, that has brought us computers that play chess, robotic vacuums and mowers, highly automated production facilities, search engines like Google, commercials with Watson from IBM providing predictive elevator maintenance, the curious and often unsatisfying interactions with Apple’s Siri interface and even the remarkable big data management that has powered Amazon’s explosive growth and enabled SpaceX to land its first stage rocket components. But smart technology has still been changing the fabric of society at about the same, ever-increasing pace of other technological changes.

Then OpenAI released ChatGPT as a free tool on November 30, 2022, in preview mode. At the end of 2024, just over two years later, Apple, Google, Microsoft and almost all other major tech companies have incorporated similar generative AI into the tools we all use today. Trained on vast amounts of publicly available information, AI like ChatGPT is changing how businesses operate, forcing a reevaluation of work practices, upending the way software is written and developed, business content is created and all manner of ideas are generated. Roles that have only ever been enhanced by technology are under threat of being supplanted by AI. Educators are grappling with an upheaval in how education happens and what it means for students to create, teachers to teach and learners to learn.

On a similar trajectory, facilities organizations are exploring how they can utilize AI to accelerate the work around content creation, communication with colleagues as well as people being served, and aiding of the processes within their operations.

In our research on this topic, we queried Copilot, Microsoft’s AI tool which is embedded in the Office suite of products the following question, using casual and easily misinterpreted language: “Can you explain how facilities organizations can best leverage AI?”

Very quickly, Copilot produced the following list, each with its own descriptive narrative:

- Enhanced Operational Efficiency through Automation

- Optimized Energy Management for Cost Reduction

- Predictive Maintenance to Prevent Downtime

- Data-Driven Insights

- Intelligent Space Utilization

- Safety Enhancement and Error Elimination

- Quick, Informed Decisions

- Democratizing Data for Stakeholders

- Tailored, Adaptive Solutions

- Integration with HVAC and Lighting Systems

Whether these are all available today or just can be part of AI support is very much in question. And whether the ideas here meet an agreed upon definition of AI is worth considering as well. Copilot and similar tools are growing better every day at leveraging the material that they have been taught on to generate remarkable, useful lists like these. But how does it translate to the facilities management realm?

This winter we issued a survey on current AI practices in higher ed facilities organizations. Across a number of survey questions, several valuable insights arose.

Looking forward? Almost 29% of respondents indicated that they aspire to have AI overseeing the operations of buildings and systems at some point in the future. An additional 42% were more cautious with a “maybe.”

These data points are reflections on the rate of adoption in facilities organizations and the caution with which facilities organizations are leveraging AI. We are all seeing much more expansive adoption in the broader business sector, and particularly Generative AI like ChatGPT. According to a May 2024 McKinsey report on the state of AI in early 2024, 65% of respondents reported using generative AI which was nearly double the number a year previous. And according to DemandSage, in November of 2024, 40% of companies worldwide were using AI, and 82% were using or exploring its use. Whether either of these survey driven data points are entirely accurate, they indicate a wider adoption in businesses that can readily adopt available AI tools into their businesses right now.

Finally, the Gordian survey pointed to challenges in adoption that are not surprising. A lack of skills in-house was the reason for 31% of respondents to be slow to move forward with AI, while 28% indicated no clear ROI in the face of so many other competing pressures. And 22% indicated that an inability to integrate with existing systems was a major hurdle. For each, it is evident that the incorporation of AI will require a change in people and/or systems that seems onerous given other pressing operational expectations.

Leaders are leveraging AI to alter their organization’s work when it can help advance productivity and streamline efforts. Yet in a business so connected to the physical, it remains unclear how much it can or will ultimately alter the operational work. What actions and decisions can be made without actually being in the space, seeing the physical conditions and challenges that embody the built environment these organizations are responsible for shepherding? And how does an AI tool even garner the information to be used to make decisions since it is privately held inside the organizations we are talking about?

Impact For Facilities Organizations

These AI tools were developed using the vast amount of information that was made available on the internet and various other dedicated sources. Knowing those sources of information is key to some important thinking about the implications for facilities organizations.

So far, AI is being used for facilities organizations in much the same way it is doing so with any other business enterprise. In the ways that we can all take advantage of general knowledge, AI brings ready access to what feels like an endless amount of information that extends beyond our own individual grasp. Want to write a formula in Excel for an action you haven’t done before? Just ask Google’s Gemini to write a formula in lay language and it will respond with a viable answer that will often work using functions you may have never seen before. Or it will at least be close and with a little more back and forth, you can create the successful formula.

Want a starting place for next week’s team meeting? Lay out the issues you want to discuss and Microsoft’s Copilot will reply with an organized agenda, topics and even guidance on what to pay attention to or what to try to avoid. Or per the Copilot suggested facilities applications for AI above, provide ChatGPT key information on spaces and occupant loads and hours of operation and the right direction, and it will crunch the numbers for you to optimize the use of those spaces. AI works like a partner to help us expand our access to information we don’t readily have at our fingertips (like a search engine) and interacts with us in an almost human fashion to create accelerated solutions to problems we might pose.

Still, it is a partner with limitations. Dean Stanberry, Past Chair of the International Facilities Management Association, notes that you “shouldn’t ask ChatGPT anything in a realm you don’t understand already.” Why? He goes on to say that, “Each output is limited to that conversational experience. If you know enough to be able to clarify and edit and sound like the author, then you are starting to optimize it.” In other words, don’t assume that the Excel formula you were given is right if you don’t know what a correct result is going to look like in the first place. It’s how we would act with our human colleagues so why should we treat AI differently?

A key hurdle for realistic use in facilities organizations is making sure the needed data for utilizing AI is available to the tool you are using. These large tools we have been talking about are general language models and there are limitations based on what they have been given access to. If the subject is not in the realm of information it has been trained on, an AI cannot help.

For facilities professionals this can become very real, very quickly. A simple question like “What should I do when the -80°F freezer alarm in Sage Hall is tripped?” is not one that ChatGPT can readily answer. It can provide answers about possible responses to a freezer alarm in the way that a YouTube video can be called upon to offer assistance for tying a bowtie. But it can’t address your specific situation. It doesn’t have the right information to help you address this problem for the researchers in your community.

But what if it did? With the potential available via AI to act smarter, what should we do? What should our goals be?

One goal is self-managing buildings. Buildings that know what they need, when they need it and can call out for help at such times. Benchmarkable buildings that can compete with each other, learn from each other and optimize their own performance in service of the people and the systems inside them would be a tremendous step forward, according to Emmanuel Daniel. He is the Founder of Alosanar and formerly with Microsoft where he was the Global Head of Smart Buildings and also Digitization Lead for its data centers. He has worked across the globe designing and building some of the world’s smartest buildings.

But such self-management won’t happen quickly, he cautions. “We don’t have great high quality building data yet, like we do for the large language model behind ChatGPT.” That information is locked up on your campus, in the buildings and perhaps in the building automation systems that you might be utilizing. He noted that at Microsoft, one of the most technologically advanced companies in the world, they have more than 300 data centers globally and more than 125 buildings at their Redmond, WA campus. These assets have immense amounts of critical equipment. Yet an asset inventory and deep dive into the specifics of the assets and how many of each type they have and the origins of the assets would take a considerable amount of time. If information as basic as “how many buildings we have, what type, how are they performing and are they efficient or not” is not instantly available, we are a long way away from those self-managing buildings.

Campuses do already utilize building automation systems with ever greater connectivity, but those systems still rely immensely on supervised learning and labeled data sets to provide predetermined decisions on the select information that is available within a given building. And for good reason. Building automation can have great consequences. The wrong action with a valve or a damper might freeze a building in winter or drive mold deep into a building in summer; it could destroy someone’s research or ruin a one-of-a-kind manuscript. Not to mention it might make people miserable.

But to train an AI to help us think through problems, we need more data; data that isn’t readily available today. Sensing what is happening in the environment and making it readable/knowable/usable is not simple. It remains quite expensive to provide monitoring for each data point to be gathered and then transfer it back to the system for processing. The capabilities of these automation systems are limited by our willingness to invest in gathering the data. And the willingness to share it.

To teach AI to understand and act appropriately for facilities, an AI tool must be given access to millions of data points, from many millions of square feet of space, over myriad use and environmental conditions in order to build up the capacity for AI to engage in building operations. Daniel sees the need for a dedicated team that can extract, normalize and qualify the data, build the learning models and the train the model, just like was done with these other AI tools. It will take years and millions of dollars.

But the payback could be immense. Because the cost of mistakes is so high, there are significant redundancies in all systems to make sure that the right choices are made by layers of people involved. If those people can be brought into a situation where there is sufficient trust in the data, many decision points could be offloaded to AI and people freed up to handle customer concerns directly and address truly novel functional issues in the field.

Dr. Russell Garcia, Industry Director, Higher Education at Johnson Controls, notes that their organization recognizes the opportunity for AI learning that exists with their vast data, but also sees the limits of even their vast dataset.

“It is a very high priority in our organization, but it will take significantly more effort to reach a place where the data can be fully leveraged.”

Cleaning the data and bringing it all together for one tool to learn from and then be able to apply in a wide array of circumstances is a massive effort.

The challenges to moving forward with AI in the facilities realm isn’t deterring everyone, though. At Penn State, they are developing several AI tools to complement the work performed by the facilities team. In addition to using a widely deployed space sensor tech to establish a deeper understanding of space utilization and overall movement across campus, they are using AI to make HVAC alarms across multiple systems more intelligent and building a chatbot for internal use by their service team to strengthen the work order process.

The team at Penn State has deployed robust alarm management tools to connect countless different building automation systems and get a handle on the myriad alarms that happen routinely. Acting as an integrator and shared interface, this allows the facilities team to leverage AI to provide early diagnostic behavior, determine if the alarms are false and, when not, initiate a series of steps, up to and including getting work orders and emergency response actions underway. In the case of the chatbot, they are collaborating with on campus student resources to build a tool for service desk personnel to scour all available building information data sets (service histories, maps, building drawings, etc.) and establish background as well as possible alternative responses to a potential work order.

With both of these closed source, large language models (AI tools based on data that is not publicly available), they are using Penn State data exclusively to train AI tools about typical activity on campus, allowing the model to learn as it goes and then start to engage with future demands in a fashion that will supplement and improve the work activity of already busy facilities personnel. In both cases, Tom Rodgers, Interim Associate Vice President for Facilities Management and Planning, notes that “you can’t take these tools as built and move them to another campus. It’s going to be too specific and will not be able to respond to another campus’s needs.” But the approach certainly could be.

Rodgers is adamant that waiting for others to create the right tools for your campus has costs you can’t afford. “Now is the time to think differently about your future. Don’t be afraid of the technology. It’s going to enhance what you are doing and will make your decisions better, today.”

Engaging AI

Consider the following five ideas as you are exploring the use of AI:

Patience: The need to act now is necessary because the establishment of AI tools in the facilities world will take time. As you innovate, be prepared for a longer journey than many may expect and setbacks along the way. Fortunately, facilities organizations are full of people who have the patience to work through a deliberative process. It is important to make sure everyone inside AND outside the organization is kept up to speed on activity so that they can see the progress you are making and share in your enthusiasm.

Skill: Fundamentally, is your team interested in engaging with AI or is your organization not yet prepared for this new technology? If they are not ready, you must first develop a pathway toward their acceptance and identify low risk areas (the simplest of robotics for example) for them to explore the idea of technology changing their work practices. If your team is interested, can you create space and time in their work day for experimentation and education? If you are fortunate to have people literate and comfortable already (or are in a position to hire that skill set), you must still make space in their work to allow for the development and the rollout of the new tools, systems and processes.

Application: Develop a list of places and processes where you believe you and your team could be doing things more effectively if your tools were better. Be sure to quantify the benefits. Next, decide whether the improvements you want to make are simple repetitive tasks which you would like to see offloaded or if they are decision making improvements that will accelerate and enhance the work of your team. This will shape the types of AI you will engage, if it is even AI at all. Quantifying the benefits will help with convincing your team and the rest of the institution to support you with implementation.

Data: Determine if there is information available to empower your proposed changes. Is there an existing AI-driven tool that has all the information necessary to address your needs? If not, do you have the data to train the tool that you will need to have built or even build yourself?

Support: Identify partners across the campus who share your enthusiasm and can help you with successful implementation. Seek support from leadership that can control your budget and are willing to provide the resources to achieve the improvements you expect. Establish partnerships with those who will benefit from the changes you will make and will have the patience to work through your experimental efforts. And perhaps seek support from those who can help publicize the innovative spirit of your organization, to help accelerate the adoption of your successful initial efforts across the broader institution.

In Ethan Mollick’s highly informative and clarifying book, “Co-Intelligence: Living and Working with AI,” released just a year ago, he notes that even with all of this change brought on by AI, it is very unclear which science fiction future we are headed into. In his conclusion, he muses about four scenarios: #1 – As Good As It Gets posits that the growth in AI capability is over. #2 – Slow Growth suggests that the exponential change slows to something more familiar. #3 – Exponential Growth offers a future that remains full of change at the current pace for the foreseeable future. And with #4 – The Machine God, AI reaches equivalency with humans in its capability and then moves beyond us. Each scenario asserts that AI is here with us and only in one dystopian view do we find ourselves grappling with a child of our creation that goes on to have the capacity to dominate or benevolently look over humans. But in each scenario, he reminds us that the best outcomes will arise only if we step forward to join in the creation of the future that will serve us best.

The data we report from our work across the country serves to acknowledge where our campuses have been, and to articulate the situation campuses find themselves in today. Nathan Grawe’s observations are so powerful because of the call on the rare information that is both a record of the past (birthrates over time) and very accurate predictor of the future (18-year-olds in years moving forward). Ethan Mollick’s speculation for the future provides reasonable approaches to engaging with a tool that everyone recognizes will be utterly transformative. Finishing this document where we started, we are reminded that this information is in our hands to guide our choices going forward, and it remains only to be seen whether we will act or be acted upon in creating that future that will serve our communities best.

This document is a collaborative work that leans upon the collective efforts of nearly everyone on the planning team at Gordian to gather, qualify and validate the information used herein. But several people in the organization warrant special acknowledgement for their contributions to making this actual report come together. Tiffany Smith, Sophie Mason and Donnie Vittorelli were all involved in scrubbing and analyzing the data in aggregate to ensure that what is represented here is the most accurate information available from our database. Without their work, there would be no aggregated data set from which we are able to draw these conclusions. We are all grateful for their efforts.

Share this: